There are a few other guidelines that support the need foradjusting entries. Other methods that non-cash expenses can be adjusted through include amortization, depletion, stock-based compensation, etc. This is extremely helpful in keeping track of your receivables and payables, as well as identifying the exact profit and loss of the business at the end of the fiscal year.

- It is not worth it to recordevery time someone uses a pencil or piece of paper during theperiod, so at the end of the period, this account needs to beupdated for the value of what has been used.

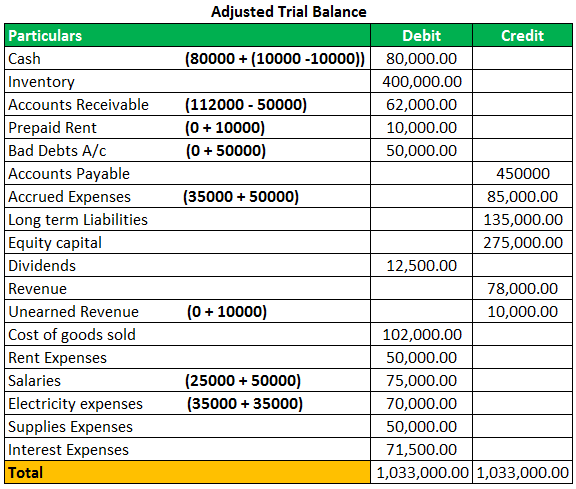

- You have your initial trial balance which is the balance after your journal entries are entered.

- For instance, if a company forgets to record accrued wages at the end of the period, the expense will be understated, and net income will appear higher than it actually is.

- Let’s say a company has five salaried employees, each earning$2,500 per month.

- An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability).

Example of an Adjusting Journal Entry

Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others.

Balance Sheet

At the end of the accounting period, the unearned revenue is converted into earned revenue by making an adjusting entry for the value of goods or services provided during the period. Accruals are adjustments made for revenues that have been earned but not yet recorded, and expenses that have been incurred but not yet paid. For instance, a company may have provided services in December but will not receive payment until January. An accrual entry ensures that the revenue is recorded in December, aligning with the period in which the service was provided. Similarly, if a business incurs an expense in one period but pays for it in the next, an accrual entry is necessary to reflect the expense in the correct period. This method adheres to the matching principle, which states that expenses should be recorded in the same period as the revenues they help generate.

What is the approximate value of your cash savings and other investments?

You will notice there is already a credit balance in this account from the January 9 customer payment. The $600 debit is subtracted from the $4,000 credit to get a final balance of $3,400 (credit). This is posted to the Service Revenue T-account on the credit side (right side). You will notice there is already a credit balance in this account from other revenue transactions in January.

This can happen when estimates are not updated or when they are based on incorrect assumptions. To avoid this mistake, it is important to review and update estimates regularly. We now record the adjusting entries from January 31, 2019, for Printing Plus.

The following Adjusting Entries examples outline the most common Adjusting Entries. For example, the business might pay its rent quarterly in advance, when paid the amount will have been debited 2020 review of xero to a prepaid rent account in the balance sheet. At the end of each of the next three months adjusting journal entries are made to record the amount of rent utilised during the month.

Adjustment entries are an essential aspect of accounting that helps ensure the accuracy and completeness of financial statements. These entries are made at the end of an accounting period to correct errors, omissions, and discrepancies in financial transactions. He does the accountinghimself and uses an accrual basis for accounting.

Non-cash expenses – Adjusting journal entries are also used to record paper expenses like depreciation, amortization, and depletion. These expenses are often recorded at the end of period because they are usually calculated on a period basis. This also relates to the matching principle where the assets are used during the year and written off after they are used. The rent for the month of 3,000 has been transferred from the prepaid rent account in the balance sheet, to the rent expense account in the income statement. Making adjusting entries is a way to stick to the matching principle—a principle in accounting that says expenses should be recorded in the same accounting period as revenue related to that expense.